Washington supports central Europe’s energy security, says Szijjártó

October 24, 2014BBC: Ukraine voters to pass verdict on pro-Europe politics

October 25, 2014

There’s some interesting discussion points in the UK-based Absolute Return Partners October 2014 Letter, by Niels C. Jensen, most of which I agree with, others not.

Japan-Style Deflation in Our Backyard?

It is no secret that we have been long-standing believers in deflation being a more probable outcome of the 2008-09 crisis than high inflation. What has changed over the past six months is that the world has begun to move in different directions. Whereas rising unit labour costs in the U.S. make outright deflation in that country quite unlikely, the same cannot be said of the Eurozone.

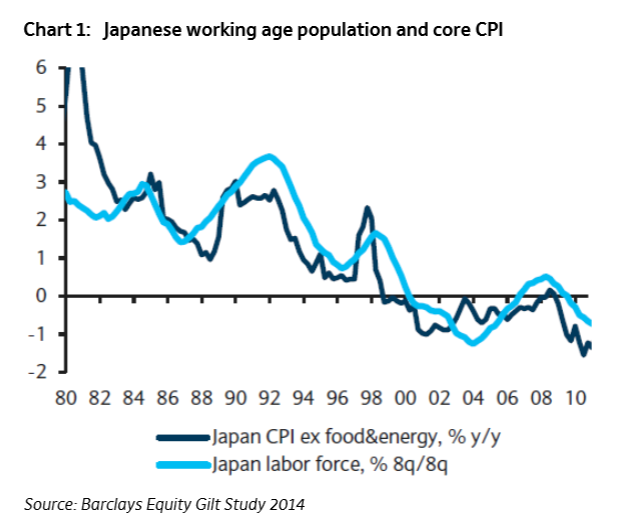

Japan-style deflation across the Eurozone is no longer an outrageous thought. As you can see from chart 1, there is a close link between CPI and demographics. That has certainly been the case in Japan and I don’t see any reasons why it should be any different in Europe. The negative demographic trends are perhaps not as acute in Europe as they were in Japan in the early to mid 1990s, so one might expect a less dramatic outcome here, but the writing is on the wall. Furthermore, Japan’s problems were multiplied due to an almost complete lack of political recognition and willingness to take drastic action. At least, with Mario Draghi in charge of the ECB, there seems to be a willingness to do something.

Deflation and “Willingness To Do Something”

Jensen is mistaken about Japan’s willingness to take action. Japan has a debt-to-GDP ratio of 250%, highest of any major developed country, as a direct consequence of fighting deflation.