Huge brawls in legislatures, explained

October 14, 2014

Europe Forsaken in ETFs as Record Money Pulled on Economy

October 14, 2014

Although the SP 500 (NYSEARCA:SPY) shrunk by a mere 5.2% from the high on September 18, the chatter on the street is that the “correction” is back on, which is a repeat of the message broadcast in early August that subsequently vanished as the market raced higher. Some even offer reasons as to why the market topped, and that is the beauty of the First Amendment. I watched Mohamed A. El-Erian speak on “Sunday Morning Futures” with Maria Bartiromo and he gave three reasons for the recent market volatility: poor economic data out of Germany; policy bickering in Europe; and the IMF’s downgrade of global economic outlook. The first two are very real, but since when do investors listen to the IMF? Either he knows and is not telling, or vice-versa. I’m tempted to say that I, single-handedly, caused the market decline with my statement that “‘we the people’ are not coming to market” on September 22. Nah!

First we received rate hike relief from Yellen’s lips on September 17, after the 10-year yield had risen from 2.35% to 2.60% in 30 days, and the market celebrated Janet’s message although the dollar kept shooting for the moon while the 10-year yield declined to 2.30% as of October 10. Needless to say, currencies respond to interest rates, and the argument can be made that the U.S. economy’s strength is driving the dollar, while declining rates create a puzzle because if the economy is strong there’s no need for low rates. On the flip side, we have the euro which continues to shrink, and that is due to either a weaker Eurozone economy, the expectation of QE from the ECB, or both. Certainly markets are extremely muddied and are a reflection of the interference by central banks around the world, and, as an example, here’s proof of the Fed’s state of confusion, to be polite, as put forth by Stanley Fischer.

“It looks like the markets have it right, somewhere in the middle of the year,” Fischer said today at an event in Washington. Still, like his colleagues, he stressed the Fed’s message that the outlook for policy is data-dependent.

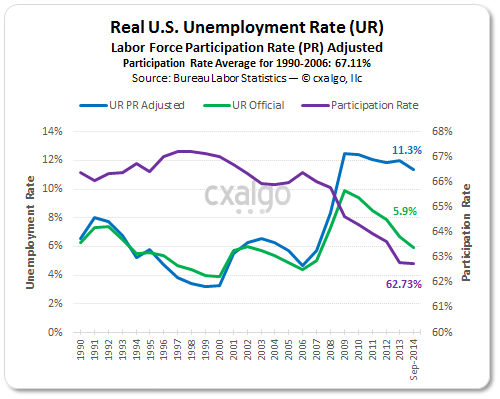

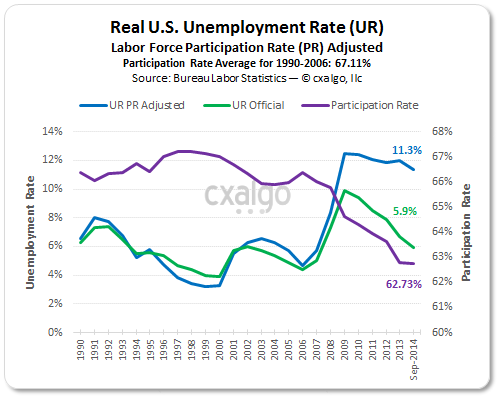

Let’s not forget that besides QE, the fed funds rate has been at zero for six years, but what exactly was Mr. Fischer saying? That he knows that economic data will justify a rate hike in 2015, or that the market may have it wrong because he’s not sure about the data? Why does every statement include a caveat? Ah, yes, I had forgotten that the unemployment rate is below Bernanke’s magic trigger of 6.5%, and it was in February of 2013 that Bernanke stated the following:

With the jobless rate in January at 7.9 percent, Bernanke said his “reasonable guess” would be that it will take three more years before the unemployment rate reaches 6 percent. Late last year, the Federal Reserve said it would keep interest rates low until unemployment reached about 6.5 percent.

The unemployment rate is now 0.6% below target and two years have passed, but maybe they’re looking at the chart below, and “Saturday Night Live” should be paying more attention to the Fed, because they’re a great source of material.

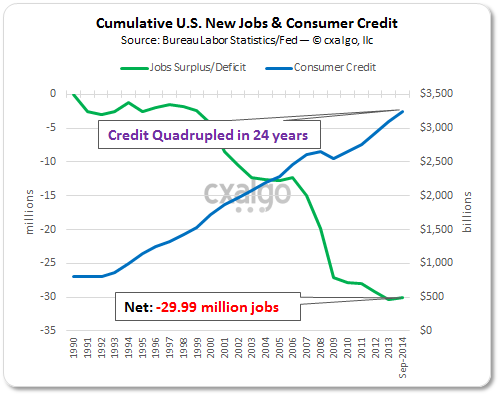

I know that plenty of explanations have been given about the unemployment condition, from demographics to bird migration patterns and planetary alignments, but we have a structural problem that transcends all politics and is best illustrated by the chart that follows.

There’s a deficit of 30 million jobs in the U.S. of A. that developed over the last 24 years as it relates to population growth, while consumer credit quadrupled, and despite what now appears to be a minor credit growth blip after the housing mania, we’re reaching for those credit limits once again. Excluding mortgages, thus far we have about $10,000 in consumer credit — credit cards, autos, student and personal loans — for every man, woman and child in America. So much for deleveraging, and something must give, especially as incomes are not keeping up with the Joneses. How does more credit drive the economy when we’re still pushing our creditworthiness to the worthless precipice with no measurable results? I suspect that a lot of credit usage is directed to making ends meet, and at some point ends will cease to meet.

But back to the market, and the “surprise” came when the Fed minutes were released, which was nothing more than what Yellen had already stated, although concerns about the dollar’s strength and global economics was voiced. The market rose nonetheless, and that’s where technical analysis comes in, but I will not bother anyone with voodooism. For amusement purposes, I wish that the FOMC minutes were provided 24 hours after the meeting as a court reporter’s transcript. In short, the Fed is in a trap of their own making because they believe that they have healing powers, and the Fed is the perfect mascot that replaced the quarterback in an economic team on a losing streak.

As a side note, there’s one school of thought, or lack thereof, which I shall call Botox Economics, that advocates the distribution of cash directly to the population instead of QE. That is utopia, and we shall wipe out all recessions henceforth and no penalty for excesses, inefficiency, and risk shall ever be imposed. When the core principles fail, please rewind and play again under a different title!

Along comes Mario Draghi and delivers a speech at the Brookings Institution on October 9, and while he’s praised for his unique jawboning power — “whatever it takes” — he’s short on QE specifics, or QE altogether, American style.

Let me be clear: we are accountable to the European people for delivering price stability, which today means lifting inflation from its excessively low level. And we will do exactly that. The Governing Council has repeated many times, even as it was adopting new measures: it is unanimous in its commitment to take additional unconventional measures to address the risks of a too prolonged period of low inflation. This means that we are ready to alter the size and/or the composition of our unconventional interventions, and therefore of our balance sheet, as required.”

But this time his words weren’t as soothing, and market players abandoned ship, at least temporarily. Keep in mind that QE in the Eurozone is illegal by all measures, but that shouldn’t stop the bureaucrats from going forward with it, and the large bet has been that the ECB will buy all the sovereign bonds that have been accumulated thus far, driving, for example, Spanish rates below U.S. 10-year treasuries. Draghi spoke at the International Monetary and Financial Committee the following day and tried to offer some consolation to no avail and the “within its mandate” reference should have been “legal or not.”

Our unconventional measures, more specifically our TLTROs (Targeted Longer-Term Refinancing Operations) and our new purchase programs for ABSs and covered bonds, will further enhance the functioning of our monetary policy transmission mechanism and facilitate credit provision to the real economy. Should it become necessary to further address risks of too prolonged a period of low inflation, the ECB’s Governing Council is unanimous in its commitment to using additional unconventional instruments within its mandate.

There’s still a glimmer of hope, and while the Germans are opposed to buying government debt from their southern neighbors, their mind could change when the upcoming trouble is more visible. It is complicated, with liquidity also being a problem because if the above doesn’t pan out, who will buy the debt from the holders while the European condition deteriorates. Maybe they’ll have to sell other assets to make up for the shortcomings in the sovereign debt bet . This time is different, indeed, and a cool head can see that there are too many variables, and when someone calls a top or a bottom, they’re essentially looking for attention and love. Question is whether central banks can afford for markets to drop, destroying the wealth effect mantra. But what can they do about it? That will be a test of their much advertised omnipotence.

I mentioned recently how a P/E of 5 looks to be historically cheap, and although I am not calling for that to happen simply because I don’t have a crystal ball and I’m not a zoologist, it would mean at least a 70% drop from here. And I say at least because a future P/E of 5 would be based on whatever lower earnings would be produced. For those that think that a 70% drop is extremely insane, think Japan 1989! Between December 1989 and March 2009, the Nikkei 225 declined 81.9%, a period spanning 20 years with plenty of opportunities to buy the dip. Although it has doubled since 2009, the Nikkei is still 60% below the record. Rest assured that plenty of people retired and passed away without ever recovering their hard earned money.

In simple words, a Japanese citizen that started with the equivalent of $1 million at age 45, ended up with $181,000 at age 65, although dividends may have saved the day! You think? Word to the wise: Keep in mind that prices drop first, and dividends are reduced later, and maybe that’s why investment banks have trading desks, not investment desks! Whatever pleases you, and I shall reiterate that this is not our parents’ market.

I read a comment where the individual stated that he/she would never sell anything because millions would be owed in taxes. My experience tells me that if one has millions, one doesn’t talk about it, and sometimes the options are limited: pay taxes or give it back to the market. Not trying to be a wise guy, but rather to point out how that one must always question everything until it makes sense regardless of source — yours truly included — especially as it applies to younger, impressionable people. However, most of them will tell me to go kiss a frog because they know better. How do I know? That’s exactly what I told my dad until the day that I caught myself repeating the same advice to my daughter. I guess common sense never dies, and the cycle shall repeat for millennia to come.

I was walking my dog and met a nice lady, and after a quick exchange of pleasantries she opined that I should change the collar for a harness because the dog could choke. I smiled, and replied that the dog will only choke if it’s stupid and, to the best of my knowledge, no dog has ever committed suicide. She was puzzled! This event goes back to questioning everything — a.k.a. critical thinking — and not taking every bit of information at face value.

Lastly, and for those wondering about my gold position, it is still intact and nursing a 15% loss, exacerbated by the leveraged position in ProShares Ultra Gold (NYSEARCA:UGL) and mitigated by call writing. Once again, I’m not a gold bug, and inflation, which has no relation to the price of gold, is not the driver, but rather the continually evolving geopolitical conflicts which will set the Middle East ablaze, while Ukraine has faded from the news and was only a distraction as predicted. Putin’s game of power through energy, not ideology, may not be going as planned. In addition, the Iranian nuclear negotiations may be postponed yet again, a rerun of “I Secretly Love Nukes,” which has Israel on its toes. The only added observation regarding fanaticism inspired conflict, and I hope that I’m dead wrong, is that it may extend to the streets of Europe and America for obvious reasons.

Disclosure: The author has no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it. The author has no business relationship with any company whose stock is mentioned in this article.