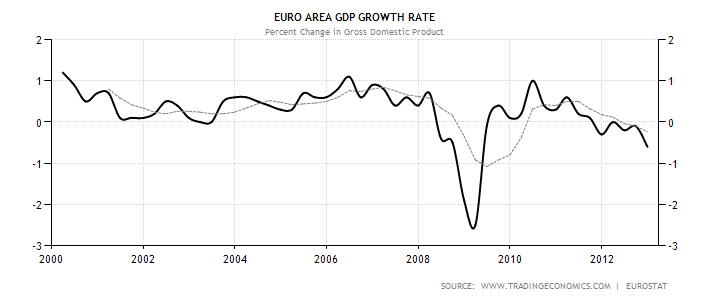

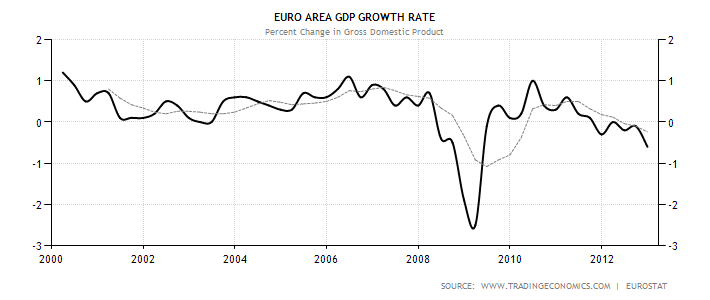

Most who follow the news know that Europe’s economy has not been growing well. As a matter of fact, Europe’s growth has been so poor that it makes the U.S. economic growth engine look outright stellar. Over the last 12 months the euro zone economy has grown by 0.15%, with the reported 2nd quarter GDP growth rate stagnating at 0.0%. This is not a short-term trend. It’s been 15 years since the euro zone last saw GDP growth above 1% on a sustainable basis. Why is Europe stuck in a slow/no growth environment?

A plethora of reasons surround the economic stagnation in Europe, including:

- Inflexible labor laws

- Bad demographics

- Decentralized banking/governmental bureaucratic/political system

- Dysfunctional currency system

- Over-reliance on the welfare safety net

The issues go on from here – but you get the picture. Many of the problems which have led to slow growth in Europe are not cyclical in nature – rather, they are systemic and self-imposed. Economic growth in Europe has been so low for so long that the main focus of many political/economic leaders continues to be worries of deflation pressures rather than a build in inflationary pressures. Low inflation is currently part of the economic landscape on a global scale, but is particularly acute in Europe.

Mario Draghi Announces New Monetary Measures

With this economic backdrop, Mario Draghi– the President of the European Central Bank (the European equivalent of our own Janet Yellen) – announced monetary actions which are to start in October. The popular press is calling these actions WIT2 – the second round of “Whatever It Takes.” While not exactly a round of quantitative easing, the actions resemble the U.S. version of Quantitative Easing, where money is “printed” and shoved into the banking system in an attempt to jump-start demand for capital though a number of mechanisms.

My conclusions as to the changes we may see from the ECB are:

- The ECB will purchase up to $1.3 trillion (1 trillion euro) in bonds from the market which are backed by loans to the real economy. This will provide fresh capital to the banking system as many banks will be able to restructure their balance sheets by selling their dicey credits to the ECB for cash.

- 2. The ability of the European banking system to start making more loans will be enhanced. Initially, this will probably have little effect on demand for capital. Loan demand will probably remain fairly lackluster, with the new, excess banking capital spilling into the public financial markets.

- An expansion in the asset-backed market will be necessary in Europe – this is the transmission mechanism that will make the actions become reality. The ECB has announced a partnership has been formed with Blackstone (a U.S.-based securities manager/underwriter).

- This action should be positive for the periphery debt markets and European corporate debt as interest rates continue to come down. The action should lead to a weaker Euro in relation to the U.S. dollar, with a push to the upside in European exports, particularly in weaker economies.

- If successful, the program should eventually push economic activity to the upside and revive inflationary expectations to a limited degree. The catalyst of the inflation revival would be the expectation that money “printing” to this degree normally does lead to some type of inflationary pressure. This would be considered a positive development since Europe has teetered on the brink of deflation for some time.

Long Term or Short Term Benefit?

As has been the case in the U.S., when a central bank starts to “print” money through radical QE-type activities, the immediate injection of excess liquidity into an economy initially lifts asset values as the money has to go somewhere. If the real economy doesn’t need or want the liquidity, it tends to flow into the capital markets (both stocks and bonds), raising prices. We have witnessed this in the U.S. on three occasions since 2009 as our own Federal Reserve performs QE activities.

However, as is the case in the U.S., long-term benefits from QE actions are questionable. We don’t yet know the final ramifications of the Fed’s radical QE activities but, eventually we will witness the results. At any rate, I don’t believe QE activities carry long-term benefits but, act as a shot of adrenaline to an economy, an injection Europe sorely needs.

Summary – Overall Thoughts on Investments in Europe

Bottom line, we expect the European-based capital markets (stocks and bonds) to start performing better than has been the case, particularly in relation to the U.S. capital markets. In many of our recent writings, we have made the strong case that a number of the foreign stock markets are undervalued in relation to U.S. equities. We have been waiting for a catalyst that may start to unlock that undervaluation – perhaps, we now have that catalyst with Draghi’s expansionist plans for the ECB.

–

The views expressed are for commentary purposes only and do not take into account any individual personal, financial, or tax considerations. It is not intended to be personal legal or investment advice or a solicitation to buy or sell any security or engage in a particular investment strategy.