Opinion: Europe needs more positive examples of reform

August 27, 2014Athletes Gain Life Skills Through YOG Culture And Education Program

August 29, 2014

This is the second of four posts about VoxEU’s e-book on secular stagnation. The first is here.

One version of the secular-stagnation theory, which posits that the U.S. and Europe may face an era of slow growth and persistently high unemployment, says that a surplus of savings over investment has lowered the equilibrium real rate of interest. This is the price that keeps saving and investment in balance. The usual mode of adjustment isn’t working because nominal interest rates in the U.S. have fallen to zero and can’t fall any more — as they’d need to, for balance to be restored. The result is a chronic shortfall of demand.

This is a plausible partial account of the crash and its precursors. The chapter in the VoxEU collection by Olivier Blanchard and colleagues at the International Monetary Fund explains that saving in the emerging-market economies, especially China, increased in the years leading up to the crash. Adding to the downward pressure on interest rates was a global increase in the demand for safe assets such as U.S. Treasury securities. China and other emerging-market economies bought safe assets in great volume to hold as reserves; this bid up their price and lowered their yields.

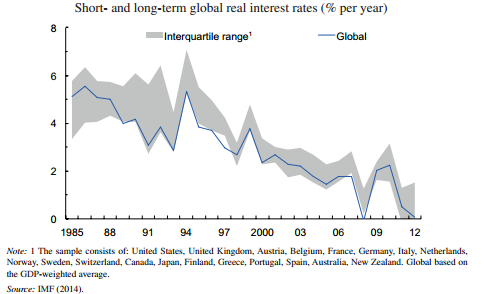

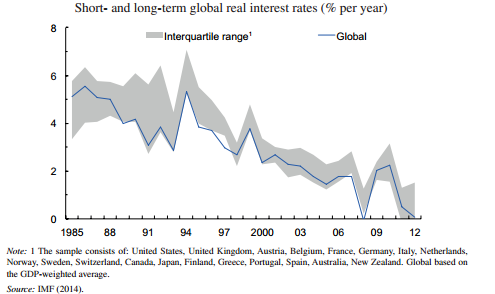

This phenomenon helps to explain the fall in real interest rates in the years before the crash (see chart). But what about the future?

Blanchard and colleagues argue that the saving-investment imbalance may persist. For one thing, in many countries, including the U.S., a continuing legacy of the crisis is heavy public and private debts. As long as households, firms and governments are striving to borrow less, saving will stay up. The demand for safe assets may stay high too: Another legacy of the crisis, say the authors, is tighter financial regulation, which, among other things, makes banks hold more safe assets.

Stronger investment demand may not come to the rescue. With confidence beaten down after the crash, it hasn’t strengthened much. After previous financial collapses, it has stayed low for years. All in all, the saving-investment imbalance could possibly even get worse.

Things don’t have to turn out this way. Emerging-market saving could fall, for instance. China’s government says it wants to rebalance the economy in favor of consumption. Reserve accumulation might slow, reducing the demand for safe assets. Business confidence could recover more strongly after all. Nonetheless, until these healthier trends are apparent, the risk of secular stagnation obliges policymakers to contemplate unorthodox policies.

Quantitative easing, as undertaken by the Federal Reserve, is one example. Think of it as an imperfect way to ease monetary conditions even when the nominal interest rate is zero.

Higher public spending and/or lower taxes — heavy public debt notwithstanding — would be another. Under the topsy-turvy conditions of secular stagnation, borrowing costs nothing; and bigger budget deficits would probably reduce the ratio of public debt to output, as Larry Summers and Brad DeLong have demonstrated. In this one respect, you could say that secular stagnation is actually a blessing — as Blanchard and colleagues put it, “Bad news for monetary policy, but good news for fiscal policy and debt overhang.”

Most radical of all, central banks could adopt higher inflation targets and use QE to announce their determination to hit them. Why would that help? At 2 percent expected inflation, a nominal interest rate of zero is a real rate of minus-2 percent; at 4 percent expected inflation, it’s a real rate of minus-4 percent. Higher expected inflation, in other words, would let the real rate fall farther — far enough to bring saving and investment back into balance.

The political obstacles to most of these options are obvious. As a result, the secular-stagnation hypothesis may be tested too thoroughly. And if this scary experiment is carried to conclusion anywhere, it’s likely to be in Europe. The VoxEU chapter by Nicholas Crafts shows that the risk of secular stagnation is far higher there than in the U.S.

The euro area offers perfect testing conditions. For one thing, unlike the Federal Reserve, the European Central Bank hasn’t yet used QE. It’s been saying that it might for many months — and its president, Mario Draghi, encouraged further speculation along those lines in his recent speech to the Jackson Hole central bankers’ conference. But even if the ECB finally tries QE, it will have to do so within tight legal constraints and with hostile politicians ordering it to stop.

The Fed has given itself more headroom on inflation. Without formally raising its target, it has let investors understand that inflation can run a little above 2 percent for a while, as well as a little below. The ECB’s target says “close to, but below” 2 percent. Moreover the Fed has a dual mandate: It’s been told to worry about employment as well as inflation. The ECB’s mandate is more single-minded.

Europe’s fiscal position is far worse as well. The European Union labors under the self-defeating provisions of the Stability and Growth Pact, which commit euro-system members to tighten fiscal policy even as the recovery stalls. Many euro-area economies had heavy debts before the crash. They lack the capacity, acting alone, to borrow more now without causing investors to panic. Joint action could deal with that, but there’s no sign of it: The fiscal pact, indefensible under these circumstances, remains an article of faith. To complete this dismal picture, Europe has worse demographics than the U.S. and slower growth in productivity.

Is secular stagnation, as Crafts puts it, “hypochondria or far-sighted prediction”? Chances are, Europe will answer the question.

To contact the author of this article: Clive Crook at ccrook5@bloomberg.net.

To contact the editor responsible for this article: James Gibney at jgibney5@bloomberg.net.